Esta es la cita con la que suelo abrir mis seminarios.

¿Es malo? En realidad no, ya que esto es exactamente lo que crea el bombo alrededor de las acciones y hace que algunas personas sean más ricas mientras que otras... bueno, no tanto.

Es lo que separa el trigo de la paja.

Lo primero es lo primero

Alibaba (NYSE: BABA), Sí, de eso trata este post, de tener la bendición y la maldición de operar a través de un régimen que no es particularmente conocido por su mentalidad abierta y liberal, pero que se dirige a la mitad de la población del planeta Tierra tal y como lo conocemos y con efectos indirectos sobre la otra mitad, me refiero a efectos sobre los consumidores.

Desde su salida a bolsa en EE.UU., el valor ha sufrido altibajos durante la mayor parte de los últimos 9 años, cada vez por motivos diferentes.

La última fue sobre Hormiga - una empresa que se vio obligada a retirar su cotización en 2020 debido a “problemas regulatorios” y en la que Alibaba tiene una participación del 33%, por lo que es una decisión que apunta a la propia Alibaba.

Una mala noticia a la que sigue otra aún peor sobre la exclusión de la bolsa de valores de Nueva York de los valores chinos, que es lo que los hace tan populares después de todo.

¿El resultado?

Una empresa con un valor intrínseco de $250 por acción, según los cálculos de la hoja de Damodaran (un libro de este distinguido autor que tuve el placer de utilizar como libro de texto principal durante muchos años en mis enseñanzas de finanzas corporativas en colegios privados en un pasado no tan lejano), acabaron siendo los olvidados, de los que no se habla.

Puedes echar un vistazo a su gráfico sin florituras a continuación y comprobarás que desde su máximo de $320 en 2021 hasta su mínimo de $63, había perdido 80% de su valor. La venta excesiva se produjo, como era de esperar, en torno a ese mínimo de $63, cuando se intensificaron los rumores sobre su exclusión de cotización, los llamados “analistas” comenzaron a dar objetivos de precios en torno a $50 (como si una caída de 80% no fuera suficiente para sus hambrientas historias de caza de clics) y, por supuesto, Alibaba no parecía una acción tan sensata para poseer en absoluto en ese momento (la misma historia con el S&P 500 en el mínimo de 2174 en la venta posterior a Covid, por cierto).

Otra cita que utilizo para cerrar mis seminarios, esta vez, es que para que usted consiga una sobrerentabilidad a largo plazo, tiene que pagar el precio de una volatilidad intermedia excesiva, con caídas a menudo de dos dígitos. Una que sin duda hará que otros se deshagan de sus acciones y no tengan que mirar atrás. Mientras tanto, puedes protegerte con opciones y técnicas de gestión del riesgo, pero hablaremos de ello en otro artículo.

Justo ayer, 4 de enero de 2023, se anunció “repentina e inesperadamente” que después de todos estos insoportables meses de espera, Ant está obteniendo una aprobación para aumentar su base de capital, por lo tanto, apuntando a normas laxas y un futuro más brillante.

Alibaba, y otros valores chinos, registraron una subida de +14%.

Antes de eso, y antes de cualquier noticia, la acción estaba rondando la región $86 - $92, acumulando efectivamente para esta ruptura. ¿Por qué acumular?

Porque su comportamiento, incluso en el último minuto, pretendía asustar a los impacientes. Se podía ver un +5% un día, y un -4% al día siguiente, sólo para ser seguido por un +3% al día siguiente. El último día antes de la ruptura, la acción abrió de nuevo en positivo, con la intención de asustar un poco, no apto para pusilánimes. Se podía observar la compra ocasional en las caídas cada día y su resistencia a pesar de que el S&P cayó 300 puntos durante el mismo periodo (diciembre de 2022).

¿Cuál será la situación en el futuro?

Pues bien, Alibaba ha allanado el camino para alcanzar a corto plazo su máximo de $120 de julio de 2022, y es de esperar que vuelva a situarse en torno a $85 para que pueda formar a largo plazo Cabeza y hombros invertidos formación que luego le dará un precio previsto de $170 grosso modo.

¿Por qué necesitamos esto?

Porque si sube en línea recta, obedecerá la regla de a vuelta a la media y como su ascenso será pronunciado, finalmente sucumbirá a la gravedad y volverá a su media, de forma tan abrupta como su ascenso.

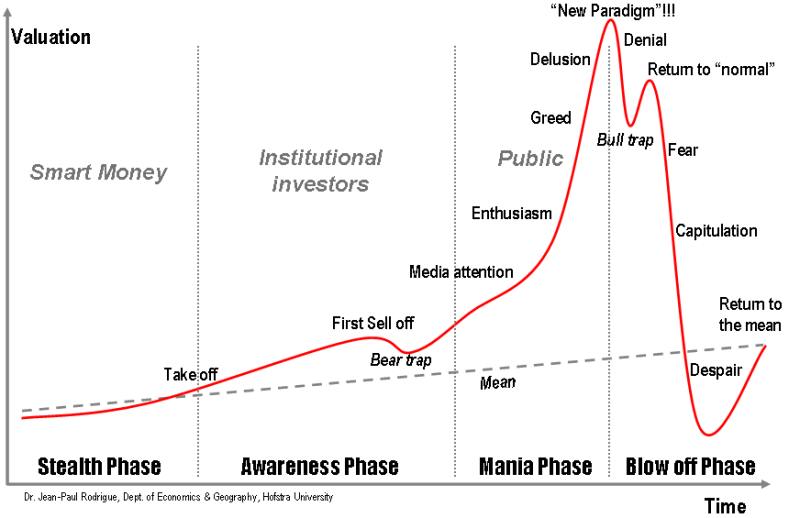

Cuestionario: Echa un vistazo a los dos gráficos adjuntos, uno es Alibaba en el transcurso de los últimos 5 años y el otro es un popular, internet de origen, gráfico de la psicología del mercado durante los ciclos.

Yuxtaponga estos dos gráficos y dígame si ve alguna diferencia....

Hasta la próxima....